Question:

If my association files a tax appeal on behalf of all unit owners in our development, am I at risk of losing my Senior Freeze exemption?

Answer:

No. The filing of a tax appeal will never cause you to lose the senior freeze. But, it could look that way.

Here’s why.

The Senior Citizen Assessment Freeze (the Freeze) provides an exemption (a deduction off the tax bill) for qualifying seniors that is about equal to the increased tax on the home from a base year to the current year using current tax rates. The base year is the year before the senior first qualified for the Freeze. So, this effectively freezes the taxable value (EAV) of the home at the level of the base year. In a rising market, that is a good for taxpayers as their taxes are based on a low value from the past rather than the higher value of the present.

If your Association filed an appeal and the assessment of your property was reduced, but your EAV remained higher than in the base year, you will receive a senior Freeze exemption this year and the tax this year will be the same as it would have been had no appeal been filed.

But, if your Association filed an appeal and the assessment of your property was reduced below the base year EAV, your senior Freeze exemption this year will be $0. This makes it appear as if you lost the Freeze, but that is not the case. If you applied for the Freeze this year on a timely basis, you remain eligible for it even though the exemption amount is $0.

If your assessment (EAV) is reduced below your previously frozen Base, your will receive a new Base that will be adjusted below the old/higher one. Your will continue to enjoy this reduced base for so long as you continue to qualify for the Freeze. In this case, you will benefit from the Association’s appeal for years to come.

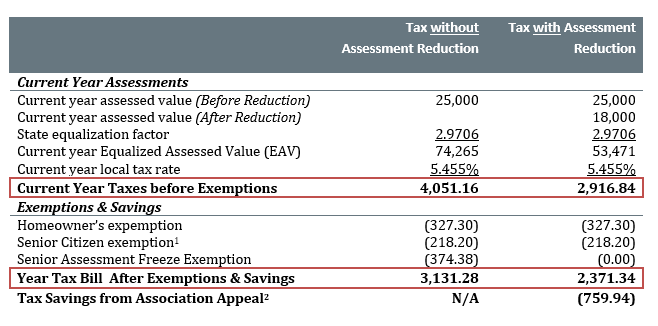

Please see the next page for a numerical example of how the Freeze works:

In summary:

- An assessment appeal will never cause the senior’s tax bill to increase.

- An assessment appeal will never cause the senior to lose the Freeze.

- A senior will lose the Freeze if the senior’s household income rises above $55,000 per year, or the senior fails to apply for the freeze each year on a timely basis.

- An assessment reduction from an Association appeal may cause the Freeze exemption (the deduction off the tax bill) to shrink, but it will never cause the tax bill to increase.

- If an assessment (EAV) is reduced below the Base, the Freeze Exemption will be $0 that year, the senior will save money that year, the Base will be reduced permanently, and the senior will realize a tax savings for so long as they remain in the Freeze program.

1Assumes the senior first obtained the Freeze in 2010; that the assessment in 2009 was $20,000; that the original Base was 67,402 (2009 assessment of 20,000 x 2009 State Equalization Factor of 3.3701); and, that the new Base has been reduced to 53,471 (2001 assessment of 18,000 x 2011 equalizer of 2,9706). In this case, the Senior Assessment Freeze Exemption is $0 because the Base has been lowered from 53,471 to 67,402.

2Tax Savings from Association Appeal is the difference between your Current Year Tax Bill After Exemptions & Savings With the Assessment Reduction (2,371.43) Current Year Tax Bill After Exemptions & Savings Without the Assessment Reduction (3,131.28). The client received an additional savings of 759.94from the appeal.